In 1928 the Screen Actors Guild decreed: ‘An Award of Merit in the form of the gold statuette trophy of the Academy (Oscar) shall be conferred annually for the following achievements:

ACTING: Performance by an actor in a leading role.

For the ability to move financial markets substantially by his words alone, this year I’d suggest the members nominate Jerome Powell.

At the end of November 2021, Jerome Powell suggested the word ‘transitory’ no longer applies in describing the inflationary trend in the US economy.** The Federal Reserve have also signaled the end to quantitative easing and the willingness to raise interest rates but again have not said anything regarding exactly when or by how much.

In the meantime, Wall Street forecasts for Federal Reserve rate hikes have changed from a range of between zero and two hikes for 2022 in November to currently between three and SIX in 2022.

Fed rhetoric has caused fairly dramatic moves in global financial markets. US Treasury bond rates have staged a sharp move higher. The US 2-year yield is up 70 basis points, and the 30-year yield is up 54 basis points. Keep in mind one thing, to date Jerome Powell and the Fed haven’t actually done anything, it’s all only positioning at this point.

In all markets the true measure of value (and lack of value) comes down to one thing, price. So how has Chairman Powell’s remarks and the hawkish Fed rhetoric of the past 2 months affected financial markets?

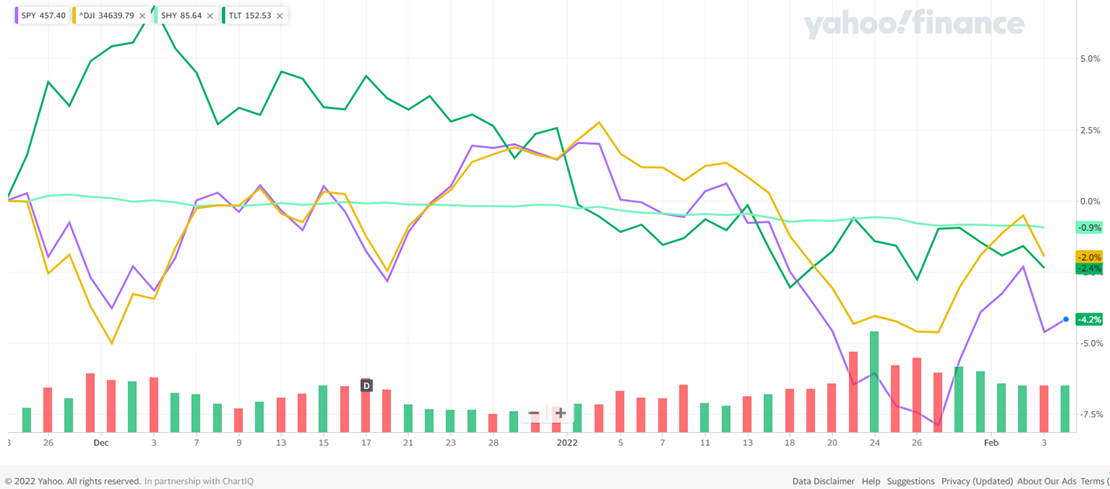

Since the end of November, the S&P 500 (purple line above) is down 4.2%, the Dow Jones Industrial Average (gold above) is down 2%, SHY (1-3 year US Government Bond ETF – light green) is down 0.9%, and TLT (10-30 year US Government Bond ETF – Dark Green) is down 2.4%. These are meaningful corrections but by no means are they dire moves.

How about more speculative investments that may be built more upon ideas than cash flows?

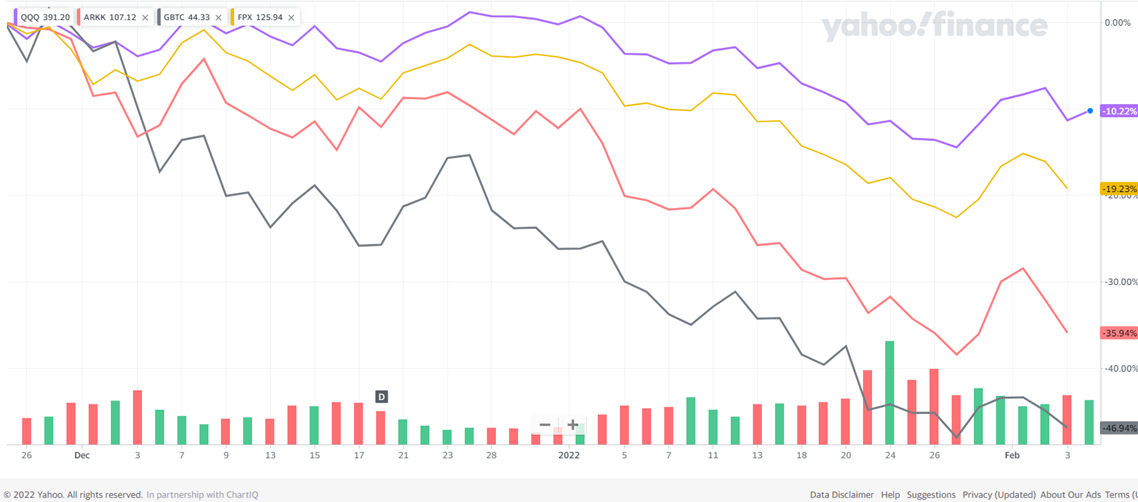

See below. The tech-heavy NASDAQ 100 ETF (QQQ – purple line) is down 10.2%, the First Trust IPO Index ETF (FPX – yellow) is down 19.3%, Ark Innovation ETF (ARKK – Red) is down 36% and Grayscale Bitcoin Trust (GBTC – Grey) is down 47%.

Certain tech stocks, IPO’s, ‘stocks of the future’, and cryptocurrencies have indeed had incredible runs in an easy money environment and have suffered a meaningful correction. The question is, what is their value in a tighter moneyed world?

What’s the point here?

Jerome Powell and the Federal Reserve have succeeded, thus far, in words alone to tighten financial conditions taking the froth off the more speculative parts of the markets. The argument could be made that this is in fact a well-orchestrated removal of excess leverage from the financial system.

Great Performance thus far.

Mind you, they will in fact be changing policy going forward and the current hand-wringing centers around the question “will it be overdone?”? There is an argument that “the Fed always overshoots” and that their future path of tightening will squeeze off the current economic expansion.

Here’s the problem for policy makers; they are flying a plane with backward looking instruments; economic indicators rarely look forward and have a time lag, so concerns of overshooting or ‘doing too much’ are justified.

So, the debate between ‘overshoot’ and ‘undershoot’ currently boils down to one thing: Inflation Fears.

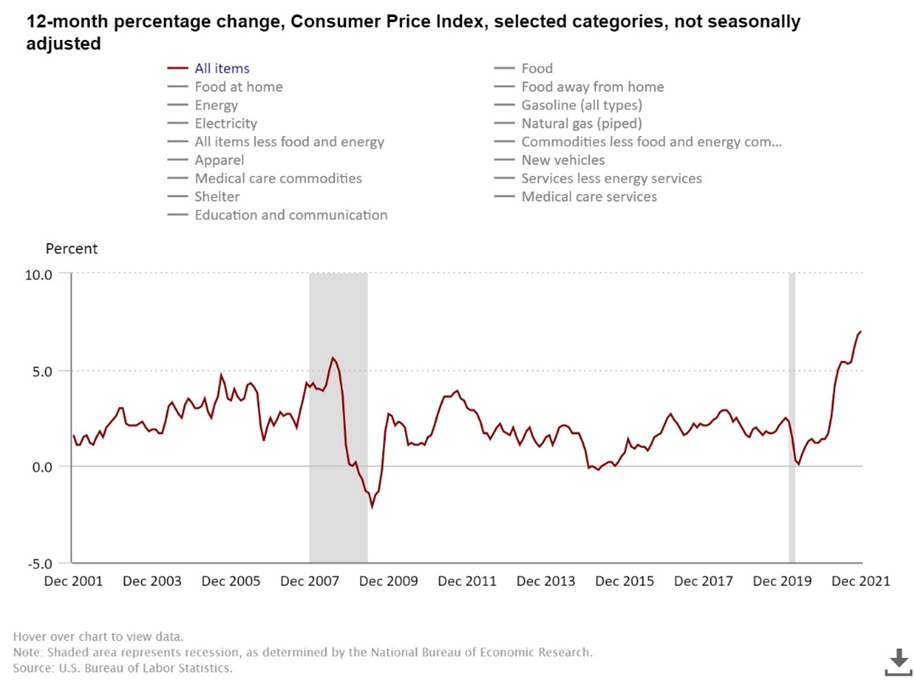

The CPI print of 7% for December 2021 (see below) was an eye-opener for financial markets, magnifying the sensitivity to any comments by monetary authorities, and it could be argued Chairman Powell has played this situation to his advantage.

January inflation numbers are due out this week and markets will study this release carefully for any change in inflation trends.

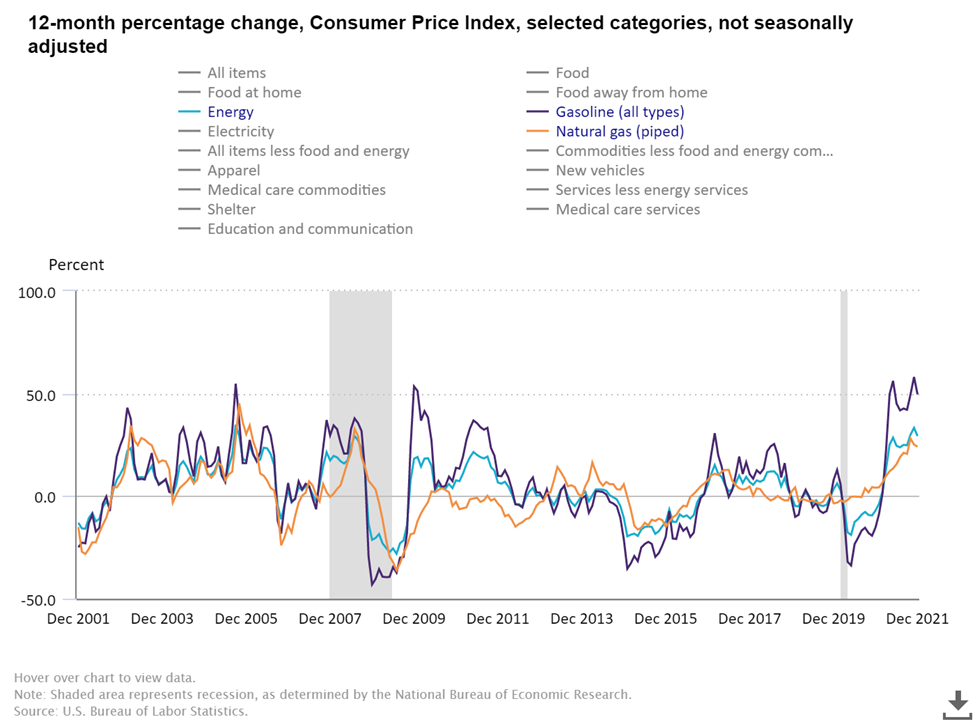

Some inflation categories to keep in mind:

- Gasoline is up 49% year over year

- Natural Gas is up 24%

- New Vehicles up 11.8%

- Food is up 6.3%

Any mitigation of these rates of inflation will be bullish for all risk assets, any extension of this trend will present the Fed with some tough decisions going forward.

We sit at this inflection point with imperfect navigational instruments and uncertainty at many levels. This is the point where proper risk management can keep you in the market even during volatile times. Consider that the Chinese characters for the term ‘Risk’ or ‘Crisis’ consists of the character for Danger and the character for Opportunity.***

Here’s a few-real time points you can consider when you look at the Dangers and Opportunities in current financial markets and the current economy:

1 - The Covid Pandemic shows signs of waning.

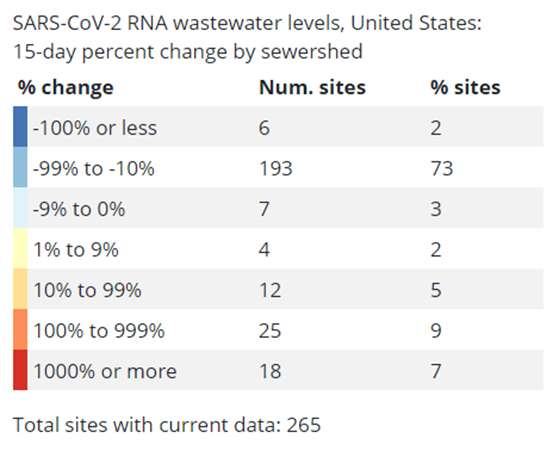

Covid 19 control measures are slowly starting to lift as virus levels are declining rapidly. The CDC reports 75% of wastewater sites reported a decline of 10 to 100% in virus levels over the last 2 weeks:

https://covid.cdc.gov/covid-data-tracker/#wastewater-surveillance

This is very promising as the tracking of this data set can provide authorities with a real time reflection of Covid in the local population. I would like to sincerely thank those who collect this information as I for one could never do so.

The process of re-opening has been and will be lumpy and volatile but the potential lifting of these Covid lockdowns and other constraints could bring about a surprising levelling out of price shocks as supply chains are re-created and re-enforced.

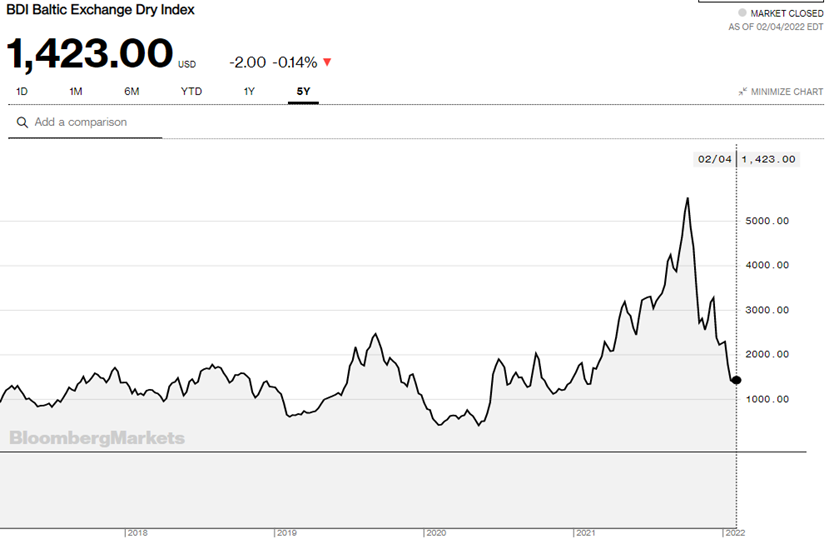

2 - So, what about supply chains? Consider the Baltic Dry Index.

The Baltic Dry Index is a measure of dry bulk shipping costs across 20 major global shipping routes. It is a leading indicator and after spiking at the start of the pandemic, is back down to a pre-covid range:

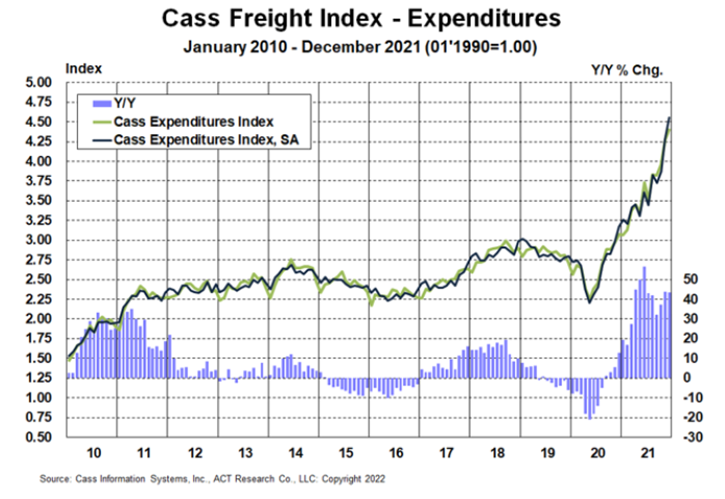

Does this mean the Global shipping and transportation costs are all at pre-covid levels? Nope. US land-based freight costs are literally off the chart:

But the Baltic Dry had a similar spike earlier and fell off dramatically. Is dry bulk shipping a leading indicator of the direction of US freight prices? Maybe. They are all links in a chain. A lowering of freight rates would have a meaningful impact on the lowering of inflationary pressures.

3- China needs to re-open.

The Olympics were probably more disruptive to supply chains than we think. A proper showing on the global stage is an imperative for Chinese authorities and until the closing ceremonies on February 20th expect China to remain constrained. There is also an argument for a rapid re-opening of the China supply chain once the Olympics end.

This fall, Xi Jinping is expected to petition the National People’s Congress to be elected leader-for-life. I know if I were running for leader-for-life I’d want my economy to be fully open and running smoothly. We may see a sharp turnaround in Chinese production and logistics fulfillment this spring and summer before the fall meeting. Both the end of the Olympics and the NPC meeting buildup could go a long way to mitigating global inflationary pressures.

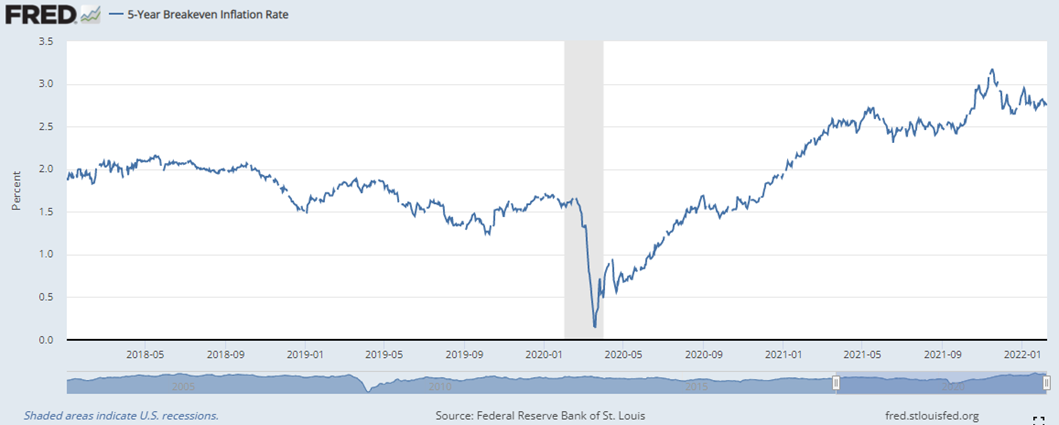

4 – The US credit market doesn’t think there will be runaway inflation.

There’s a thing called an ‘inflation breakeven’ in the bond market. It adds and subtracts a bunch of stuff to come up with what bond market participants think inflation will run over a certain period of time. The current 5-year breakeven inflation rate is 2.75% (see below). Yup, that’s less than half the current CPI print of 7%. Moreover, it is lower than the 3.17% breakeven print the week before Chairman Powell made his November comment about non-transitory inflation.

Why is this? It may be that the bond market has a high level of confidence that the Fed will combat this inflationary menace. It also may be that the market expects an overreaction to the inflation threat which will squeeze off economic growth and trigger an economic slowdown, bringing interest rates back down again. It also might mean, dare I say it, the bond market really thinks this inflation is transitory and Chairman Powell was right all along.

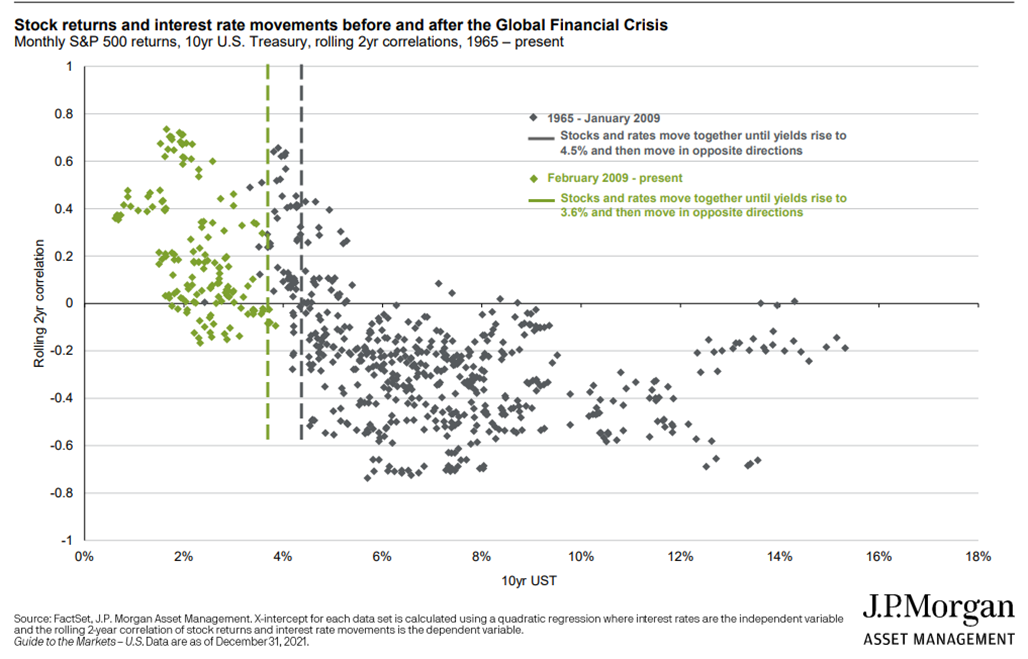

5 – Just because rates are going up doesn’t mean stocks are going down.

This great chart by David Kelly and the Guide to the Markets people at JP Morgan shows that, in a rising rate environment, stocks tend to go up until the US 10-year yield rises above 3.6% where the relationship then breaks down.

The US 10-year bond currently yields 1.97% so if this relationship holds in the current environment we still have ample room for equity market expansion.

This whole drama unfolding in the financial markets could have a most ironic ending; what if, after all the hand wringing of inflation spikes and supply chains and conflicts galore, what if inflation ends up truly being transitory? Chairman Powell and the gang can hike rates a few times this year, start winnowing down the balance sheet, and allow economic growth to proceed in a less fettered manner?

That would truly be an Oscar winning performance.

So what does one do in this nervous market?

- Participate. Cash is an option, all cash is not. The opportunity cost of not participating in the growing of financial assets can be crippling when one plans for later in life. Even if it’s only 20% of your investable assets, put something to work.

- Dollar Cost Average. It is a great way to mitigate volatility over time. I do it with client accounts constantly.

- Look for assets that don’t move together. It’s called non-correlation and these days it’s hard to find.

What are we doing at Haddam Road?

- Overweight Energy – why? See below. Energy prices have gone straight up since the pandemic washout and will remain high for an extended period, that might be the subject of another note.

- Financials – lifting of the Fed’s financial repression allows for the financial sector to start lending again.

- Consumer Staples – a great place to find solid companies that have been around forever and know how to operate in different economic environments.

- Allocating to non-correlated assets like Gold (don’t roll your eyes Millenials), Volatility, Farmland, and yes a teeny-tiny bit of crypto. Blockchain will be a formative technology, I just don’t know where and how yet.

- Bonds - with this back-up in rates it is actually worth starting small allocations to fixed income again.

It is my hope that this provides a different perspective than you might see in this space and that you gained something from your time spent.

I enjoy working with clients who want to understand their finances and be actively involved in shaping their financial future. Please email me at brian@haddamroad.com if you have any questions or comments.

Change Happens. Let us help manage your precious capital and prosper through that change.

Brian Kearns, CPA/CFP®

Haddam Road Advisors

Certified Public Accountant

Certified Financial Planner™

Registered Investment Advisor

1603 Orrington Ave, Suite 600

Evanston, IL 60201

Ph: 312 636 3067

www.haddamroad.com

NOTE: This is being provided for informational purposes only and should not be construed as a recommendation to buy or sell any specific securities. Past performance is no guarantee of future results and all investing involves risk. Index returns shown are not reflective of actual performance nor reflect fees and expenses applicable to investing. One cannot invest directly in an index. The views expressed are those of Haddam Road Advisors and do not necessarily reflect the views of Mutual Advisors, LLC or any of its affiliates.

Investment advisory services offered through Mutual Advisors, LLC DBA Haddam Road Advisors, a SEC registered investment adviser.

* - Image: https://www.flickr.com/photos/elliottcowand/49749829657v

** - https://www.reuters.com/article/usa-fed-instant/feds-powell-floats-dropping-transitory-label-for-inflation-idUSKBN2IF1S0

*** - thank you to Professor Aswath Damodaran for this excellent description of risk, his website is a treasure trove of information: https://pages.stern.nyu.edu/~adamodar/

The Why, What, and How of Financial Planning: Standards of Care and the Planning Grid

The Why, What, and How of Financial Planning: Standards of Care and the Planning Grid