With all the economic, social, and political uncertainty swirling the planet currently, I’d just like to take a moment and acknowledge what we consider to be the single best sector in terms of risk-reward for the next 12 months, the mighty US Treasury bond. And we mean the actual bonds, not a bond Mutual Fund or Exchange Traded Fund (ETF). We’ll explain at the end.

Why now? US Treasuries currently offer the exceptional combination of Capital preservation and Real Yield.

We’ll start from the beginning.

At its core, financial planning is all about managing current personal cash flows to create a surplus. It is this surplus that we invest to create and secure a future lifestyle for our clients. What are the two of the largest headwinds to this future lifestyle?

Investment loss and inflation.

Investment loss impairs the ability to compound future returns, inflation corrodes the purchasing power of future cash flows.

What do I mean?

Simply put, losses are hard to get back. Below is a table showing how much a portfolio needs to return to make up for a certain % loss:

Source: Author

Source: Author

For example, if your $1,000,000 high-risk all-stock portfolio suffers a 25% loss in a year, you need to generate a 33% return ($250,000/$750,000) just to get even. You’d need to double your account to make up for a 50% loss. That’s a lot. It’s also a real headwind to regain your future purchasing power (and fund your future lifestyle).

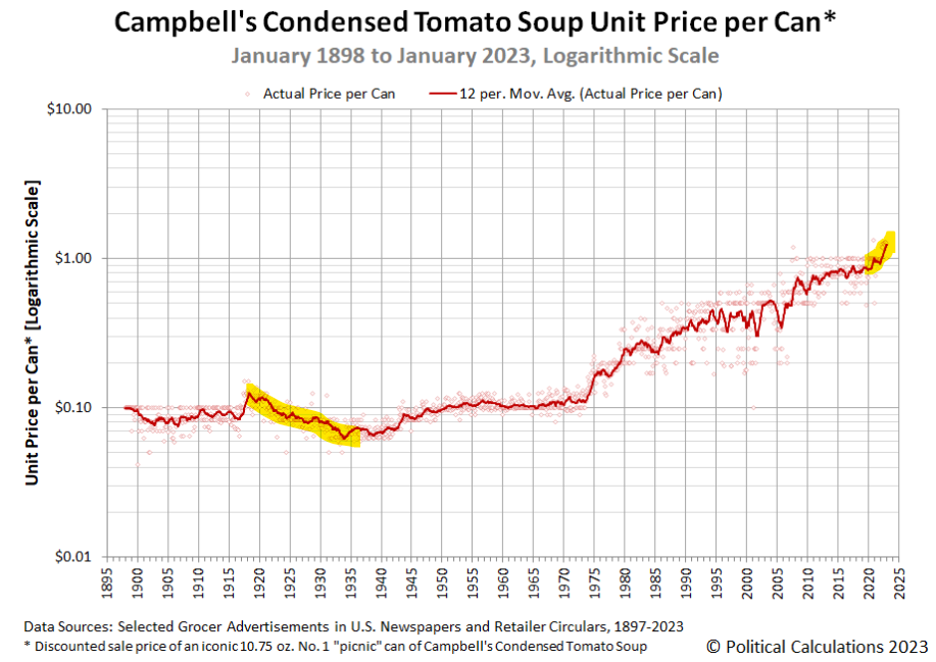

Inflation has a sneakier effect because it is not measured as easily as an investment loss, but it can be a real headwind as well. My favorite way to show the real consequence of inflation is showing its effect on the simplest of items, the price of a can of Campbells Tomato Soup:

Same old soup, higher price. 10 cents in 1898, $1.29 today. That’s inflation.

Notice the soup-spike higher since 2020; take that price change and apply it generally across the grocery store. This is the corrosive effect of inflation; a real-life consequence of the post-pandemic fiscal and monetary response of zero-interest rate policy and massive government spending.

Financial markets use a more esoteric way to measure inflation, measuring percentage changes in the Consumer Price Index (literally the price of a certain basket of consumer goods and services) as a gauge of current inflation. The current CPI measure at the time of writing is 3.7% higher than a year ago, and expectations of future CPI-inflation range between 2.9 and 3.6%.

Remember we mentioned Real Yield as an attractive thing? Any amount an investment or a portfolio earns over the rate of inflation is called the real return and specifically for bonds it is called the real yield.

When bought and held to maturity, US Treasury Bonds have virtually zero risk of loss and currently offer their best real yield in 15 years. Shorter dated bonds (less than 2 years to maturity) currently have a yield of over 5% and a real yield of around 2%. In the risk management world a 2% real yield with effectively zero risk of loss is a lot. An allocation here allows for the option of adding risk elsewhere in the portfolio and offers sound footing to build upon.

Why? Because we believe interest rates will be held higher for longer; inflation is not an easily tamed beast. Look at the Campbells Soup graph, the only time the price went down meaningfully was between 1920 and 1940 (yes, after World War One and during the Great Depression). Inflation is a money-based thing and as long as there is a super-duper amount of excess money in the economic system, inflation is not far behind.

There still is a super-duper amount of excess money in the system.

So, if we buy a short-term (less than 2 year) bond and rates go up, at maturity we will receive the bond principle back ($1000 per bond for US Treasuries) and have the option to re-invest at higher rates. If rates (for some other reasons that I will not talk about here) go down the price of our bonds will go up and we have the option of selling for a profit and allocating it elsewhere in the marketplace.

Here is a little investment management secret. If you own a bond mutual fund or an ETF (Exchange Traded Fund), the risk-reward profile we just talked about does not apply.

Why? Because you will never receive the principal of a bond at maturity. Your money is re-invested into the bond market and is constantly subject to the volatility of interest rate changes, and you have no option to reallocate those funds unless you sell the fund.

Individual bonds do have this price volatility as well, but in holding them to maturity you get your original investment back. We currently welcome the opportunity to re-allocate those funds at maturity. It is a very simple way of decreasing the risk in your bond allocation.

Talk to your current advisor, ask them about the risks in your bond allocation, if you have any further questions, please contact us. Happy to help.

At Haddam Road we are investment fiduciaries and want our clients (and the public) to understand the dangers and opportunities in the financial markets and what we are doing to manage their precious capital. After all, it is what will fund their future.

Hope this is informative, thank you for reading. Please contact me below if you’d like to talk about markets, planning, and dangers and opportunities in both.

Brian Kearns, CPA/CFP®

Haddam Road Advisors

Certified Public Accountant

Certified Financial Planner™

Registered Investment Advisor

brian@haddamroad.com

Ph: 312 636 3067

NOTE: This is being provided for informational purposes only and should not be construed as a recommendation to buy or sell any specific securities. Past performance is no guarantee of future results and all investing involves risk. Index returns shown are not reflective of actual performance nor reflect fees and expenses applicable to investing. One cannot invest directly in an index. The views expressed are those of Haddam Road Advisors and do not necessarily reflect the views of Mutual Advisors, LLC or any of its affiliates.

Investment advisory services offered through Mutual Advisors, LLC DBA Haddam Road Advisors, a SEC registered investment adviser.

IRAN: What are the risks to your portfolio?

A Roth IRA Is Not Tax-Free, It Is a Tax Swap